Pinjaman Peribadi Koperasi adalah antara produk dan perkhidmatan asas yang dibentangkan oleh beberapa koperasi pemacu di Malaysia.

Malaysia Government Loan Calculator

Adalah menjadi keputusan asas Kakitangan Kerajaan dan Kakitangan Awam yang mempunyai situasi stabil untuk memperoleh kemudahan Pinjaman Peribadi daripada koperasi berbanding dengan bank berdekatan yang juga menawarkan bantuan serupa. Secara implikasinya, keadaan semasa ini membina lagi permintaan untuk perkhidmatan Pinjaman Peribadi yang dibentangkan oleh koperasi kredit memandu setakat ini.

Ini berlaku memandangkan Bank Negara Malaysia telah memberikan garis panduan yang tegas kepada bank-bank kejiranan dalam memberikan kemudahan Pembiayaan Peribadi kepada Kakitangan Awam dan Kakitangan Kerajaan. Dengan implikasi menyukarkan pemohon untuk mendapatkan bantuan.

Ini secara implikasi mengambil kira kebimbangan yang sah bagi pemohon untuk mendapatkan kemudahan pinjaman dan pembiayaan peribadi daripada Koperasi berbanding bank berdekatan.

Berbeza dengan kemudahan pinjaman peribadi yang diberikan oleh bank berdekatan. Pihak eksekutif bank akan mempertimbangkan setiap satu daripada tanggungjawab luar pemohon dan tambahan pula semua rekod pinjaman pemohon kerana ia dihadkan oleh garis panduan yang diberikan oleh Bank Negara Malaysia kepada bank berdekatan. Secara bulat-bulat menjadikannya mencabar bagi pemohon untuk mendapatkan kemudahan Pembiayaan Peribadi daripada bank berdekatan.

Koperasi Wawasan Malaysia Berhad – Kowamas

Kowamas merupakan antara koperasi utama yang dinamik dalam menawarkan produk dan perkhidmatan Pinjaman Peribadi Koperasi kepada Kakitangan Kerajaan dan Kakitangan Awam di Malaysia. Item tersebut dikenali sebagai e-Wawasan.

Koperasi Wawasan Malaysia Berhad (Kowamas), (sebelum ini dikenali sebagai Koperasi Lepan Kabu Berhad) telah dibentangkan di bawah Demonstrasi Koperasi 1993 pada setiap tahun 1998. Persatuan asas koperasi itu kemudiannya berputar di sekitar perniagaan runcit di Kuala Krai dan Kota Bharu, Kelantan

Dengan menawarkan kadar faedah yang serius, produk e-Wawasan merupakan keputusan utama Kakitangan Kerajaan dan Kakitangan Awam dalam memperoleh kemudahan Pembiayaan Peribadi.

Koperasi Putri Terbilang Berhad – Koputri

Koperasi Putri Terbilang Malaysia Berhad atau dipanggil KOPUTRI telah didaftarkan pada 09 Walk 2006 di bawah subseksyen 7(1) Demonstrasi Koperasi 1993 sebagai sebuah koperasi penting dengan kewajipan terhad. Menjelang permulaan penubuhannya, koperasi ini telah didaftarkan dengan pendaftaran seramai 100 individu dan sehingga Disember 2018 sejumlah 17,605 individu yang mendaftar.

Antara sebab koperasi ini dibentangkan untuk memberi kemudahan kredit kepada individu kepada motivasi yang berbeza, memberi perkhidmatan tadika dan taska, latihan komuniti kos pendidikan langsung dan kelas hala tuju. Selain itu, motivasi di sebalik koperasi ini dirangka untuk melakukan latihan membeli, menjual, memindahkan hak milik, memajak, bersumpah dan menyewa, menjual dan memiliki hartanah mudah alih dan bersemangat. Koperasi juga mengambil bahagian dalam usaha bersama dan menjadi individu dengan koperasi yang berbeza untuk mengembangkan kesungguhan, pembayaran dan perdagangan maklumat koperasi.

Koperasi Bersatu Tenaga Berhad – Kobeta.

KOBETA, yang telah didaftarkan pada 22 Julai 1993, baru-baru ini dikenali sebagai KOPERASI BERSATU TENAGA MELAKA BERHAD, diselia oleh kakitangan Lembaga Kemajuan Perikanan Malaysia (LKIM) dan gabungan kaki pancing. Pada fasa permulaan, KOBETA bekerja di Melaka dan sehingga kini kem pangkalan KOBETA terletak di Melaka manakala pejabat perniagaan bekerja di Medan Tuanku, Kuala Lumpur.

Pada tahun 2004, KOBETA mendapat kod Derivasi Agensi ANGKASA untuk memperkasakannya untuk bekerja dengan pergerakan utamanya, iaitu kemudahan kredit. Dengan bantuan dan nasihat daripada YDP Koperasi UKHWAH, Datuk Hj Rahim Baba, KOBETA telah mula mengiktiraf latihan untuk pembiayaan peribadi untuk kakitangan kerajaan dan badan perundangan tanpa preseden untuk pertengahan tahun 2004. Penyusunan semula dan perubahan peraturan kecil KOBETA juga mendapat sokongan daripada Perkhidmatan Tanah dan Penambahbaikan Koperasi yang sekitar ketika itu digerakkan oleh YB Tan Sri Kasitah Gaddam.

Kami Membantu Anda

Kami sedia membantu anda dengan mengadakan mesyuarat berkaitan Pinjaman Peribadi Koperasi. Anda tidak perlu tertekan dengan alasan pentadbiran kami adalah percuma. Anda juga boleh mencari nasihat tentang membina semula dana anda. Kami tidak akan mengenakan sebarang caj pentadbiran mesyuarat kepada anda semasa tempoh pengesahan permohonan pinjaman peribadi koperasi anda.

Sebenarnya lihat kelayakan pinjaman anda sekarang.

Kami mengiktiraf permohonan pinjaman pekerja kerajaan dari negeri-negeri yang disertakan:

✓ Wilayah Perlis ✓ Wilayah Kedah ✓ Wilayah Perak ✓ Wilayah Pulau Pinang ✓ Wilayah Selangor ✓ Wilayah Melaka ✓ Wilayah Sembilan ✓ Wilayah Johor ✓ Wilayah Pahang ✓ Wilayah Terengganu ✓ Wilayah Kelantan ✓ Wilayah Sabah ✓ Wilayah of Sarawak ✓ Kuala Lumpur ✓ Government Region

A government personal loan in Malaysia or pinjaman peribadi koperasi is a type of loan that is offered by the government or government-linked companies (GLCs) to civil servants and employees of government agencies. These loans are typically offered at lower interest rates than commercial loans, and they have longer repayment terms.

To be eligible for a government personal loan, you must be a Malaysian citizen and employed by the government or a GLC. You must also have a good credit history and meet the income requirements of the lender.

Government personal loans can be used for a variety of purposes, including consolidation of debt, home renovations, medical expenses, and education. The maximum loan amount that you can borrow will depend on your income and debt-to-income ratio.

The repayment term for government personal loans is typically between three and seven years. You will repay the loan in monthly installments, which will include interest and principal.

Lower interest rates: Government personal loans typically have lower interest rates than commercial loans. This is because the government is able to borrow money at lower rates than private lenders.

Longer repayment terms: Government personal loans also have longer repayment terms than commercial loans. This makes them more affordable for borrowers, as they have more time to repay the loan.

Easier to qualify for: Government personal loans are easier to qualify for than commercial loans. This is because the government is more willing to lend money to civil servants and employees of government agencies.

You can apply for a government personal loan through the Public Sector Home Financing Board (LPPSA) or through a commercial bank.

Here are some of the best government personal loans in Malaysia:

Public Sector Home Financing Board (LPPSA) Personal Loan

Bank Islam Personal Financing-i

Affin Islamic Bank Personal Financing-i

MBSB Bank Personal Financing-i

Bank Simpanan Nasional (BSN) Personal Loan

If you are considering getting a government personal loan, it is important to compare the different loans available and to choose the one that is best suited to your needs. You should also make sure that you can afford the monthly repayments before you apply for the loan.

Government personal loan in Malaysia: A comprehensive guide

This guide will provide you with comprehensive information on government personal loans in Malaysia. It will cover everything from eligibility requirements and interest rates to repayment terms and benefits.

What is a government personal loan?

A government personal loan is a type of loan that is offered by the government or government-linked companies (GLCs) to civil servants and employees of government agencies. These loans are typically offered at lower interest rates than commercial loans, and they have longer repayment terms.

Eligibility requirements

To be eligible for a government personal loan, you must be a Malaysian citizen and employed by the government or a GLC. You must also have a good credit history and meet the income requirements of the lender.

Interest rates and repayment terms

Government personal loans typically have lower interest rates and longer repayment terms than commercial loans. The interest rate that you are offered will depend on your credit history and income. The repayment term will typically be between three and seven years.

How to apply

You can apply for a government personal loan through the Public Sector Home Financing Board (LPPSA) or through a commercial bank. To apply, you will need to provide your personal information, employment details, and financial information. You will also need to provide supporting documents, such as your salary slips and bank statements.

Benefits of getting a government personal loan

There are several benefits to getting a government personal loan, including:

Lower interest rates

Longer repayment terms

Easier to qualify for

How to choose the best government personal loan

When choosing a government personal loan, it is important to compare the different loans available and to choose the one that is best suited to your needs. You should also make sure that you can afford the monthly repayments before you apply for the loan.

Conclusion

Government personal loans can be a great option for civil servants and employees of government agencies who need to borrow money. These loans offer lower interest rates and longer repayment terms than commercial loans, and they are easier to qualify for. If you are considering getting a government personal loan, be sure to compare the different loans available and to choose the one that is best suited to your needs.

Are you looking for the best government personal loan in Malaysia?

Whether you want to purchase a car, consolidate debt or finance a home renovation project, it can be not easy to decide which type of financing will give you the most bang for your buck.With so many different types of loans out there and an array of lenders offering them, we understand how overwhelming it can feel.That’s why we’ve created this comprehensive guide that covers everything, including eligibility criteria, interest rates, application process and repayment terms, so you have all the information necessary to make informed choices when applying for a personal loan with the Malaysian Government.

Overview of Government Personal Loans in Malaysia

Malaysia offers a variety of personal loan options for its citizens, but one that stands out is the government personal loan (Pinjaman Koperasi). Through this type of financing, the Malaysian Government aims to support its citizens in achieving their financial goals and improving their quality of life.The government personal loan in Malaysia is a form of unsecured loan, meaning it does not require collateral or security. This makes it accessible to a wide range of applicants, including those who may not have assets to offer as collateral. Additionally, the government personal loan typically offers lower interest rates compared to other types of loans, making it an attractive option for many borrowers.One of the main advantages of the government personal loan is its flexibility in terms of usage. Unlike some loans that are limited to a specific purpose, such as car loans or home loans, the government personal loan can be used for a variety of purposes.This includes financing education, medical expenses, home renovations, debt consolidation, and more. This allows borrowers to have more control over how they use the funds and makes it easier to achieve their financial goals.The Malaysian Government offers longer repayment periods compared to other lenders, which can range from one to ten years depending on the loan amount and borrower’s creditworthiness. This allows borrowers to manage their finances more comfortably and make affordable monthly payment.

Advantages of applying for a government personal loan

Applying for a government personal loan in Malaysia has numerous advantages compared to other types of financing.These loans are specifically designed to cater to the needs of Malaysian citizens and offer several benefits that can make them an attractive option for those seeking financial assistance. In this section, we will discuss some of the main advantages of applying for a government personal loan.

Lower interest rates

One of the main advantages of a government personal loan is that it typically comes with lower interest rates compared to other types of loans. This is because these loans are backed and regulated by the Government, making them more secure for lenders.With lower interest rates, you can save a significant amount of money throughout your loan repayment period. This can make a big difference, especially for those looking to finance a larger project or purchase.

Flexible repayment terms

Government personal loans also tend to offer more flexible repayment terms compared to other types of loans. This means you can negotiate the loan duration and monthly payments that best suit your financial situation.You can choose between shorter or longer-term loans depending on your needs and budget. This flexibility can help you better manage your finances and avoid any potential financial strain.

Easier eligibility criteria

Applying for a government personal loan may also be easier compared to other types of loans. This is because the eligibility criteria are often less stringent, making it more accessible for those with lower credit scores or little credit history.Government loans also have set income requirements, which can make it easier to determine if you meet the necessary criteria. This can save you time and effort in the application process.

Government support and protection

As the Government backs these loans, there is a level of support and protection provided for borrowers.In case of any unforeseen circumstances or financial difficulties, the Government may offer assistance through loan deferment options or other forms of aid to help you manage your loan repayments.

No hidden fees

When applying for a government personal loan, you can rest assured that there are no hidden fees or additional charges.These loans have transparent terms and conditions, making it easier to understand the total cost of borrowing and avoid any surprises.

Accessible for all types of borrowers

Another advantage of government personal loans (Loan Koperasi Kerajaan) is that they are accessible to all types of borrowers, including those from lower-income backgrounds or with a lack of collateral.This can provide equal opportunities for individuals to access financial aid and improve their financial situation.

Requirements for applying for a government personal loan

While government personal loans have more relaxed eligibility criteria compared to other types of loans, there are still some requirements that applicants must meet. These vary depending on the specific loan program and lender, but here are some general requirements you may need to fulfill:

Malaysian citizenship

Minimum age of 18 years old

Stable income with proof of employment or business

Good credit score and history

Satisfactory debt-to-income ratio

Valid identification documents

It is important to note that meeting these requirements does not guarantee approval for a government personal loan. Lenders may also consider other factors such as the purpose of the loan, your financial stability and ability to repay, and overall creditworthiness.

A step-by-step guide to applying for a government personal loan

If you are interested in applying for a government personal loan, here is a step-by-step guide to help you through the process.First, research and compare different government personal loan options. This will help government employees and you understand the various interest rates, repayment terms, and eligibility criteria offered by different lenders.Next, gather all the necessary documents, such as identification documents, proof of income and employment, credit score reports, and any other relevant financial information.Once you have selected a suitable lender and are ready to apply for the loan tenure, you can either do so online or in person at a designated government agency or bank.When filling out the application form, make sure to provide accurate and complete information, as any discrepancies may delay the approval process.You may also be required to submit additional documents or undergo a credit assessment before your loan is approved. This is to ensure that you are financially capable of repaying the loan.Once your application is approved, carefully review the terms and conditions of the loan before signing and stamp duty act any contracts. Make sure to understand the interest rate, repayment schedule, and any other agency fee or charges associated with the loan.After signing the contract, you will receive the confirmation letter and the loan amount either through a direct deposit or check.Make sure to keep track of your loan repayments and make timely payments to avoid any penalties or additional charges.If you face any financial difficulties during the repayment period, reach out to your lender for assistance and explore options such as deferment or restructuring of the loan.

Risks associated with taking out a Government Personal Loan Malaysia

Here are the potential risks to consider before applying for a government personal financing i loan in Malaysia:

Defaulting on loan repayments

One of the biggest risks associated with taking out any loan is defaulting on your payments. This can result in late fees, penalties, and even legal action by the lender.To avoid this risk, it is important to carefully assess your financial situation and ensure that you can comfortably afford the monthly payments before taking out a loan.It is also crucial to make timely payments and communicate with your lender if you encounter any financial difficulties.

High-interest rates

While Government personal loans often offer lower interest rates compared to conventional loans, they may still be higher than other forms of rhb personal financing i such as savings or investments.This means that over time, you may pay more in interest than the initial loan amount.To mitigate this risk, it is important to shop around and compare interest rates from different lenders before making a decision. It would help if you also considered your overall financial goals and whether taking out a loan at a higher interest rate aligns with them.

Impact on credit score

Taking out a government personal loan can also affect your credit score. This is because lenders may conduct a credit check before approving your loan, and missed or late payments can negatively impact your score.To avoid this risk, make sure to only take out a loan that you are confident you can repay on time. You should also monitor your credit report regularly and address any errors or discrepancies as soon as possible.

Potential for additional fees

While Government islamic personal loans (Pinjaman Syariah) are known to have transparent terms and conditions, there may still be hidden fees or charges that you need to be aware of. This can include processing fees, early repayment penalties, or insurance costs.To avoid any surprises, make sure to carefully review the loan agreement and ask your lender about any potential additional fees before signing.

Lack of financial education

One of the biggest risks for borrowers is a need for more knowledge and understanding about personal finance. This can lead to overspending, mismanaging debt, and overall poor financial decisions.Before taking out any loan, it is important to educate yourself on basic financial concepts such as budgeting, debt management, and credit scores. You can also seek advice from a financial advisor or counsellor to help you make informed decisions.

How much interest will I have to pay?

The amount of interest you will have to pay on a government personal loan in Malaysia depends on various factors such as the loan amount, repayment term, and your creditworthiness.Typically, government personal loans offer lower interest rates compared to other forms of personal financing. This is because the Government backs them and often has stricter eligibility criteria to ensure that borrowers are able to repay the loan.The interest rate may also vary depending on the type of government personal loan you are applying for. For example, a student loan may have a lower interest rate compared to a business startup loan.To get an estimate of how much interest you will have to pay, you can use online calculators or consult with your lender. However, keep in mind that civil sector are just rough estimates, and the actual interest rate may vary based on your circumstances.It is also important to note that federal and state governments personal loans in Malaysia often have fixed interest rates, meaning they stay the same throughout the repayment period. This can make budgeting and planning for loan repayments easier compared to variable interest rates.Additionally, some lenders may offer incentives for timely or early repayment, such as lower interest rates or waived fees. It is important to inquire about these options and take advantage of them.If you are struggling with high-interest rates on your current government personal loan, consider refinancing at a lower rate. This involves taking out a new loan with better terms to pay off your existing loan.

How much can a bank loan me?

The amount that banks can loan you depends on several factors, including your creditworthiness and the type of loan you are applying for. Generally, banks will consider your income, credit score, and debt-to-income ratio when determining how much to lend you.Your income is one of the most important factors that banks will look at when evaluating a loan application. This includes not just your salary deduction but also any other sources of income, such as investments, rental property, or side hustles. A higher income can increase your chances of being approved for a larger loan amount.Your credit score is another crucial factor that banks take into consideration. This number is based on your credit history and gives lenders an idea of how likely you are to repay the loan on time. A higher credit score can help you qualify for a larger loan amount, while a lower score may result in a lower loan amount or even rejection.Banks also consider your debt-to-income ratio, which is the percentage of your income that goes towards paying off debt. This includes any existing loans, credit card balances, and monthly bills. A lower debt-to-income ratio indicates a lower risk for the bank and may increase your chances of being approved for a larger loan amount.The minimum and maximum loan amounts offered by banks also vary depending on the type of loan. For example, a personal loan may have a minimum amount of RM5,000 and a maximum amount of RM100,000, while a home loan can range from hundreds of thousands to millions.

What is a credit score? And how does it differ from a credit report?

A credit score is a three-digit number that reflects your creditworthiness based on your credit history. It serves as a measure of how likely you are to repay any borrowed funds. In Malaysia, credit scores typically range from 300 to 850, with a higher score indicating lower risk and better chances of being approved for loans.On the other hand, a credit report is a detailed record of your credit history, including all your past and current credit accounts, payment history, and outstanding debts. It also includes information such as your details, government sector employees history, and any legal actions taken against you related to credit.While a credit score is based on the information in your credit report, they are not the same thing. Your credit score is a numerical representation of your creditworthiness, while your credit report is a comprehensive record of your credit history. Lenders may consider both when evaluating a loan application, but they may also place more weight on one over the other depending on their policies and criteria.It is important to regularly check both your credit score and credit report to ensure that they are accurate and up-to-date. Any errors or discrepancies should be reported and corrected, as they can affect your creditworthiness and borrowing opportunities.

What happens if I pay my loan instalment late?

If you fail to make a loan installment payment on time, it can have negative consequences on your credit score and overall financial health. Late payments may result in late fees and interest charges, which can increase the total cost of your loan.Moreover, consistently paying late or missing payments altogether can severely damage your credit score. This can make it difficult for you to obtain future loans or credit and may also result in higher interest rates if you are approved.In some cases, lenders may also report late payments to credit bureaus, which can further impact your credit score and make it harder for you to borrow money in the future.It is important to communicate with your lenders if you are unable to make a payment on time. They can offer alternatives, such as a grace period or payment plan, which can help you avoid negative consequences.

Tips and tricks on getting the best deal when applying for a government personal loan

Here are the top tips and tricks to keep in mind when applying for a government personal loan in Malaysia:

Shop around: Don’t settle for the first lender you come across. Do your research and compare interest rates, fees, and terms from different lenders to find the best deal.

Negotiate: Feel free to negotiate with your lender for better terms or lower interest rates. If you have a good credit score or a stable income, you can negotiate for a better deal.

Improve your credit score. A higher credit score can help you qualify for lower interest rates and better loan terms. Work on improving your credit by paying bills on time and keeping outstanding debts low.

Consider other costs: Aside from interest rates, also consider other costs such as processing fees, late payment fees, and early repayment penalties when comparing loan offers.

Read the fine print: Before signing any loan agreement, make sure to carefully read and understand all terms and conditions. Pay attention to hidden fees or clauses that may result in additional costs.

Beware of scams: Be cautious of unsolicited offers or promotions for government personal loans. Always verify the legitimacy of the lender before providing any personal or financial information.

Remember, always make informed decisions and consider your financial situation carefully before taking on any loan. Overall, being a responsible borrower can increase your chances of getting the best deal and managing your loans successfully.

FAQs

What is the minimum salary to get a personal loan in Malaysia?

The minimum salary requirement for a personal loan in Malaysia varies among lenders. Generally, it ranges from RM2,000 to RM3,000 per month. Some banks may also require a higher minimum income for non-Malaysian citizens or applicants with lower credit scores.

Can I apply for more than one government personal loan at a time?

Yes, you can apply for more than one government personal loan at a time. However, it is important to consider your repayment capabilities and the impact on your credit score before taking on multiple loans.

What is the difference between a secured and unsecured personal loan?

A secured loans requires collateral such as property or savings as security for the lender in case the borrower defaults on payments. On the other hand, an unsecured personal loan does not require collateral but usually has higher interest rates to compensate for the risk. Government personal loans in Malaysia are typically unsecured loans.

How long does it take to get a government personal loan approved?

The time frame for approval of a government personal loan can vary among lenders. Some may approve and disburse funds within a few days, while others may take a few weeks. It is important to check with the lender for their specific processing time and plan accordingly for your financial needs.

By taking the time to explore government personal loans in Malaysia, you can arm yourself with the knowledge you need to make informed decisions. It is important to do this research prior to signing any loan contracts so that your finances are safeguarded and remain in a secure position.As always, we suggest looking for other alternatives before committing to a loan, as well as weighing the pros and cons of any decisions that you make. Above all, be sure not to rush into anything and take your time when considering government personal loans in Malaysia.Doing research can mean the difference between getting bogged down in debt or feeling peace of mind about your financial future. Whichever option you choose, we wish you luck on your journey to financial security – so start researching today!

Government personal loans are financial assistance programs provided by governmental entities, both at the federal and state levels, to support individuals in meeting various financial needs. These loans serve as a valuable resource for those seeking affordable and accessible means of financing their educational pursuits, homeownership goals, business ventures, or personal emergencies. Unlike loans from private financial institutions, government consumer loans often come with distinct advantages, such as competitive interest rates, lenient credit requirements, and flexible repayment terms. It often feature competitive interest rates, also known as profit rates, making them an attractive financing option for various needs.

What is The Importance of Government Personal Loans

When the Interest rate is calculated, based on factors like the base rate, can significantly impact the total repayment. To apply, simply click on the ‘Apply’ button on the bank’s website and be prepared with the necessary documents. These documents typically include proof of income and identification, e.g., your IC. Third-party institutions often handle the application and disbursement process, making it more convenient for borrowers, while considering assets and the type of personal loan, whether it’s secured or unsecured, is essential to make the right financing choice.” A personal loan is an unsecured form of borrowing, meaning it does not require collateral or asset backing. While applying for loads, some necessary documents required to get approval before click on the apply. Besides this, some third party organization also offer loads for government employees.

What is Government Personal Loans

Government personal loans (Pinjaman Koperasi)are financial assistance programs offered by government entities, typically at the federal and state levels, to individuals for various personal financial needs. These loans are designed to provide affordable and accessible sources of funding for purposes such as education, home improvement, small business development, and other personal financial requirements. Unlike loans from private institutions financial, government personal loans often come with favorable terms, lower interest rates, and more lenient credit requirements, making them an attractive option for those who may not qualify for or afford traditional loans. These loans serve to promote economic stability, address specific societal needs, and provide financial support to citizens across diverse demographics. For individuals in the government sector, the best personal loans for the government often come with competitive financing options, transparent fees and charges, and a clear privacy policy. When you apply for government personal loans, the use of Tawarruq financing principles is common, ensuring Shariah compliance and accessible financing solutions for eligible borrowers. Government personal loans are accessible to government employees and individuals employed by GLCs, offering competitive financing amounts, favorable terms and conditions, and convenient monthly payments through salary deduction, all at competitive interest rates expressed as per annum (BPA). Personal loans in Malaysia 2024, the Malaysian citizens can benefit from government personal loans, including Personal Financing-i for the civil sector, offered by BSN. These loans provide competitive financing amounts with flexible loan tenures and hassle-free transactions, ensuring affordable and accessible personal financing options for eligible individuals. When seeking personal financing in Malaysia, it’s crucial to explore various options and understand the diverse types of personal loans available. Islamic banks such as Maybank, Agrobank, and MBSB offer competitive rates based on the concept of Shariah compliance, making them appealing to many. For civil servants and employees of statutory bodies or government-linked companies, there are specific loan facilities, such as AgroCash-i, tailored to meet their income requirements. These personal loans often come with fixed and low-interest rates, ensuring affordable financing options. To find the best loan for your needs, you can use a loan calculator provided on the bank’s website and apply online, subject to the submission of required documents like a copy of your IC. Late payment charges, based on the base rate (BR), may be applicable, so it’s important to stay informed about the terms. Additionally, secured loans like mortgages or GLA may offer longer repayment periods, while unsecured personal loans constitute a convenient financing facility without the need for collateral. To learn more about the loan options, please visit the Biro Perkhidmatan Angkasa website for additional information and the third-party implementation of these programs.

Types of Government Personal Loans

Government personal loans are offered by various levels of government, including federal and state authorities, to provide financial assistance to individuals. These loans serve different purposes and come with specific eligibility criteria, interest rates, and terms. Here, we will explore the two primary types of government personal loans:

Federal Government Personal Loans

Federal government personal loans are financial assistance programs provided by federal agencies to eligible individuals. They are designed to address various financial needs and can be advantageous due to their often competitive interest rates and flexible repayment terms. Here are some key types of federal government personal loans:

Federal Student Loans: These loans are offered through the U.S. Department of Education to help students cover the costs of higher education. Federal student loans include Subsidized and Unsubsidized Stafford Loans, PLUS Loans for parents, and Grad PLUS Loans for graduate students. They typically offer low interest rates and flexible repayment options.

SBA Disaster Assistance Loans: The U.S. Small Business Administration (SBA) provides disaster assistance loans to individuals and businesses affected by natural disasters. These loans can help with repairing or replacing damaged property, covering temporary living expenses, and more.

HUD Home Improvement Loans: The U.S. Department of Housing and Urban Development (HUD) offers home improvement loans to homeowners for property repairs and improvements. These loans can be particularly useful for low-income homeowners looking to make necessary upgrades to their homes.

VA Personal Loans for Veterans: The U.S. Department of Veterans Affairs (VA) offers various personal loan programs for veterans and their eligible family members. These include the VA Home Loan program, which provides home loans, and the VA Personal Loan program, which can assist veterans with various financial needs.

State Government Personal Loans

State government personal loans are tailored to the specific needs of residents within a particular state. These programs vary from state to state and may address issues unique to the local population. Here are some examples of state government personal loan programs:

State Housing Finance Authority Loans: Many states have their own housing finance authorities that offer affordable housing programs. These loans can help first-time homebuyers, low-income individuals, and other eligible borrowers secure affordable housing options.

State Educational Loans: Some states provide their own educational loan programs to supplement federal student loans. These loans can have competitive interest rates and may be available to state residents attending in-state colleges and universities.

State Small Business Loans: State governments often partner with local financial institutions to offer loans to small businesses within the state. These loans may provide funding for business expansion, equipment purchases, and other growth initiatives.

Emergency Relief and Assistance Programs: States may also offer emergency relief and assistance programs to aid residents facing financial hardships due to unforeseen circumstances such as natural disasters, medical emergencies, or economic crises.

Popular Government Personal Loan Programs In Malaysia

Malaysia has several popular government personal loan programs aimed at assisting its citizens with various financial needs. These programs are often administered by government agencies, financial institutions, or other organizations. Please note that the availability of these programs and their specific terms may change over time, so it’s advisable to verify the latest information with relevant authorities or financial institutions. Here are some popular government personal loan programs in Malaysia:

Personal Financing-i by Bank Rakyat

Bank Rakyat’s Personal Financing-i is a Shariah-compliant personal loan program in Malaysia. It offers financing solutions for various financial needs, including debt consolidation, home renovation, education, and more. This program is known for competitive profit rates, flexible repayment terms, and minimal processing fees, making it a popular choice among Malaysians. Eligibility criteria typically include a minimum income requirement and Malaysian citizenship. The loan amount and tenure may vary based on individual profiles.

TEKUN Nasional’s Entrepreneurial Financing Scheme

TEKUN Nasional’s Entrepreneurial Financing Scheme supports small and micro-enterprises in Malaysia. It provides financial assistance to individuals looking to start or expand their businesses. The program aims to empower entrepreneurs, especially in rural areas, by offering accessible financing. Loan amounts and terms are structured to meet the specific needs of entrepreneurs. Eligibility often includes business viability assessments.

Skim Pinjaman Peribadi 1Malaysia (SP1M)

The Skim Pinjaman Peribadi 1Malaysia (1Malaysia Personal Loan Scheme) is a government initiative that offers personal loans at attractive interest rates. It targets low and middle-income individuals who may face challenges accessing traditional bank loans. The program’s aim is to provide affordable and accessible financing for various personal needs. Eligibility criteria are usually linked to income levels and Malaysian citizenship.

Yayasan Pembangunan Ekonomi Islam Malaysia (YaPEIM) Microcredit Scheme

YaPEIM’s Microcredit Scheme is designed to provide financial support to economically disadvantaged individuals. It offers microcredit financing with the goal of promoting economic independence and financial stability among marginalized communities. The program focuses on encouraging entrepreneurship and self-sufficiency. Eligibility criteria may include income assessments and alignment with program objectives.

MyBeautiful New Home Program

The MyBeautiful New Home Program is a government initiative aimed at helping low and middle-income families in Malaysia purchase their first homes. It offers financial assistance, including grants and subsidies, to reduce the financial burden of homeownership. The program’s goal is to make homeownership more accessible and affordable for eligible individuals and families. Eligibility criteria may involve income levels and homeownership status.

Higher Education Fund (PTPTN) Loans

The Higher Education Fund (Perbadanan Tabung Pendidikan Tinggi Nasional or PTPTN) provides loans to Malaysian students pursuing higher education, both domestically and abroad. These loans help cover tuition fees and living expenses during their studies. Repayment terms are structured to begin after the student graduates and start working, easing the financial burden during the educational period.

Amanah Saham Bumiputera (ASB) Loan

ASB loans are offered by selected banks in Malaysia and are secured by ASB units held by the borrower. These loans provide financial flexibility to Bumiputera investors who have invested in ASB units. Borrowers can use their ASB units as collateral to access funds for various purposes, including personal investments or emergencies.

Marriage Loans

Some Malaysian state governments offer marriage loans to assist young couples in covering their wedding expenses. These loans are typically interest-free or come with very low-interest rates, making them an attractive option for couples looking to start their lives together. Eligibility may include residency requirements and age restrictions.

How To Apply For A Government Personal Loan

Research Loan Programs

Start by researching government personal loan programs to find one that aligns with your financial needs and qualifications. You can find details about various programs on government websites or through local agencies.

Verify Eligibility

Ensure that you meet the eligibility criteria for the chosen loan program. Common eligibility factors include citizenship, income level, credit history, and the loan’s intended purpose.

Prepare Required Documents

Collect the necessary documents, which may include identification, proof of income, bank statements, and any additional paperwork specified by the program. Having these documents ready will expedite the application process.

Complete Application

Obtain and fill out the application form provided by the relevant program or financial institution. You can often find these forms on official websites, in local government offices, or at the bank handling the loan.

Submit Your Application

Submit your completed application along with the required documentation to the designated office or financial institution. Follow the submission instructions provided in the application package.

Await Approval

Government personal loan applications can take some time to process. Be patient while the program administrators assess your application, which may include a credit check.

Review Loan Terms

Once your application is approved, carefully review the loan terms, including interest rates, repayment schedules, and any associated fees. Ensure you understand and accept these terms.

Sign the Loan Agreement

If you’re satisfied with the terms, sign the loan agreement. This document formalizes your commitment to repay the loan according to the specified terms.

Receive Funds

After signing the loan agreement, you will typically receive the loan funds. The method of disbursement can vary, such as a direct deposit or a check in your name.

Use Funds Responsibly

Utilize the loan funds responsibly for their intended purpose. Misusing the funds may result in legal and financial consequences.

Follow the Repayment Schedule

Adhere to the agreed-upon repayment schedule. Government personal loans often offer flexible repayment options, so select one that suits your financial situation and make payments promptly to maintain a positive credit history.

Seek Assistance

If you have questions or encounter challenges during the application or repayment process, reach out to program administrators or financial advisors for guidance. They can provide valuable assistance and address your concerns.

Tips for Getting Approved for a Government Personal Loan

Obtaining approval for a government personal loan can be a structured process with specific requirements. Here are some tips to increase your chances of approval:

Review Eligibility Criteria: Thoroughly understand the eligibility criteria for the specific loan program you’re interested in. Different programs may have varying requirements, such as income levels, credit scores, or intended use.

Improve Your Credit Score: A higher credit score can significantly boost your chances of approval. Pay bills on time, reduce outstanding debts, and address any discrepancies in your credit report to improve your creditworthiness.

Manage Debt-to-Income Ratio: Ensure that your debt-to-income ratio is within acceptable limits. A lower ratio, where your debt doesn’t consume a large portion of your income, is generally more favorable.

Provide Accurate Information: Be truthful and accurate when completing your loan application. Any inconsistencies or misinformation could result in a denial of your application.

Steady Employment History: A stable employment history demonstrates financial reliability. Lenders often prefer borrowers with a consistent work history, as it suggests a reliable source of income.

Collateral or Co-signer Options: If your credit or income doesn’t meet the program’s requirements, consider offering collateral or having a co-signer with a stronger financial profile. This can enhance your application’s credibility.

Choose the Right Program: Select the loan program that best aligns with your financial needs and qualifications. Applying for a program for which you meet all the criteria will improve your chances of approval.

Seek Professional Guidance: If you’re uncertain about the application process or your eligibility, consult financial advisors or professionals who can provide guidance tailored to your specific situation.

Prepare Complete Documentation: Gather all necessary documents and ensure they are well-organized. Missing or incomplete paperwork can delay your application or lead to rejection.

Build a Relationship with the Lender: If you’re applying for a loan through a local bank or credit union, consider building a positive relationship with the institution. A history of responsible banking can enhance your credibility as a borrower.

Apply for an Appropriate Loan Amount: Request a loan amount that is realistic based on your income and repayment ability. Borrowing within your means can strengthen your application.

Review Your Application Before Submission: Double-check your application for errors or omissions. Mistakes can lead to delays or rejection.

Address Past Loan Defaults: If you have a history of loan defaults, work on settling or resolving these issues before applying for a new loan. This demonstrates responsibility to potential lenders.

Maintain Stable Financial Behavior: Keep your financial affairs in order leading up to and during the loan application process. Consistent financial responsibility can boost your application’s appeal.

Remember that each government personal loan program may have its unique approval criteria, so be sure to review the specific requirements for the program you are interested in. Additionally, be prepared to patiently work through the application process and address any concerns or questions that may arise during the evaluation process.

Government Personal Loans FAQs

What are government personal loans?

Government personal loans are financial assistance programs provided by government entities to individuals for various personal financial needs. These loans typically offer competitive interest rates and favorable terms.

How do government personal loans differ from traditional bank loans?

Government personal loans often have lower interest rates and more flexible credit requirements, and may not require collateral or co-signers, making them accessible to a broader range of borrowers.

Can I apply for multiple government personal loans at once?

While it’s possible to apply for multiple loans, it’s essential to consider your financial capacity and the potential impact on your credit. Applying for multiple loans simultaneously may affect your credit score.

Government personal loans are valuable resources for individuals seeking affordable financial solutions to meet various personal needs. Whether it’s funding education, improving your home, or starting a small business, these loans offer favorable terms and accessibility. Government personal loans in Malaysia provide accessible and affordable personal financing solutions for education, home improvement, and other financial needs. It play a crucial role in supporting the financial well-being of individuals, including those working in the public sector, by offering affordable and accessible financing options in Malaysia. Moreover, It available to government employees, often include competitive financing amounts and favorable terms and conditions. These loans offer the convenience of salary deductions, ensuring manageable monthly payments, while interest rates are usually expressed as per annum (BPA), making them a reliable financial solution. Understanding the eligibility criteria, application process, and tips for approval can help you make the most of these government-backed financial assistance programs. Always conduct thorough research and reach out to the relevant authorities for the latest information on available programs and their specific requirements.

Dokumen komprehensif ini menyediakan analisis yang meluas mengenai Pinjaman Koperasi Kerajaan Malaysia, yang biasanya dikenali sebagai Pinjaman Koperasi Kerajaan di Malaysia. Laporan itu menyelidiki konteks sejarah, objektif, kriteria kelayakan, proses permohonan, faedah, cabaran dan kesan pinjaman ini terhadap individu dan ekonomi Malaysia. Dengan tumpuan untuk menggalakkan rangkuman kewangan dan pembangunan sosio-ekonomi, Pinjaman Koperasi Kerajaan Malaysia memainkan peranan penting dalam memperkasa kakitangan kerajaan dan memupuk gerakan koperasi di negara ini.

Isi kandungan:

pengenalan 1.1 Latar Belakang 1.2 Objektif 1.3 Kepentingan Pinjaman Koperasi Kerajaan Malaysia

Evolusi Sejarah 2.1 Kemunculan Koperasi di Malaysia 2.2 Peranan Kerajaan dalam Memajukan Koperasi 2.3 Kejadian Pinjaman Koperasi Kerajaan Malaysia

Objektif Pinjaman Koperasi Kerajaan Malaysia 3.1 Pemerkasaan Kewangan 3.2 Menggalakkan Gerakan Koperasi 3.3 Mengurangkan Tekanan Kewangan

Kriteria Kelayakan 4.1 Kakitangan Kerajaan 4.2 Keahlian dalam Koperasi 4.3 Tempoh Perkhidmatan Minimum 4.4 Sejarah Kredit dan Kapasiti Pembayaran Balik

Proses permohonan 5.1 Dokumentasi Permohonan 5.2 Saluran Penyerahan 5.3 Proses Kelulusan 5.4 Pengeluaran Dana

Jenis Pinjaman Koperasi Kerajaan Malaysia 6.1 Pinjaman Peribadi 6.2 Pinjaman Pendidikan 6.3 Pinjaman Perumahan 6.4 Pinjaman Kenderaan 6.5 Pinjaman Kecemasan

Kadar Faedah dan Syarat Pembayaran Balik 7.1 Kadar Faedah Tetap lwn. Berubah 7.2 Tempoh Bayaran Balik 7.3 Tempoh Ihsan 7.4 Penalti Pembayaran Lewat

Faedah Pinjaman Koperasi Kerajaan Malaysia 8.1 Kadar Faedah Berdaya saing 8.2 Pilihan Pembayaran Balik Fleksibel 8.3 Rangkuman Kewangan 8.4 Kesan Sosial dan Ekonomi

Cabaran dan Kebimbangan 9.1 Liputan Terhad 9.2 Pinjaman Ingkar dan Pinjaman Tidak Berbayar 9.3 Kesesakan Pentadbiran 9.4 Persaingan dengan Bank Perdagangan

Kisah Kejayaan 10.1 Kajian Kes Penerima 10.2 Kesan terhadap Kesejahteraan Kewangan 10.3 Pertumbuhan Koperasi

Sokongan dan Peraturan Kerajaan 11.1 Peranan Kementerian Pembangunan Usahawan dan Koperasi 11.2 Rangka Kerja Kawal Selia 11.3 Insentif Cukai

Analisis Perbandingan dengan Produk Kewangan Lain 12.1 Pinjaman Bank Perdagangan 12.2 Institusi Kewangan Mikro 12.3 Pilihan Simpanan dan Pelaburan Peribadi

Prospek dan Inovasi Masa Depan 13.1 Kemajuan Teknologi 13.2 Perluasan Kriteria Kelayakan 13.3 Amalan Lestari

Kesimpulan 14.1 Kesan dan Kepentingan 14.2 Cabaran dan Peluang 14.3 Jalan Hadapan

Rujukan

Pengenalan

1.1 Latar Belakang: Pinjaman Koperasi Kerajaan Malaysia, atau Pinjaman Koperasi Kerajaan di Malaysia, ialah program bantuan kewangan yang direka untuk menyokong kakitangan kerajaan di negara ini. Pinjaman ini diberikan melalui koperasi, yang merupakan organisasi bantu diri yang ditadbir oleh ahli mereka. Pinjaman Koperasi Kerajaan Malaysia bertujuan untuk menyediakan kredit yang boleh diakses dan berpatutan kepada penjawat kerajaan, menggalakkan kestabilan kewangan dan memupuk gerakan koperasi di Malaysia.

1.2 Objektif: Objektif utama Pinjaman Koperasi Kerajaan Malaysia adalah untuk menyediakan pemerkasaan kewangan kepada kakitangan kerajaan, menggalakkan pertumbuhan koperasi, dan mengurangkan tekanan kewangan di kalangan penerimanya. Analisis komprehensif ini akan meneroka bagaimana objektif ini dicapai dan menilai kesan keseluruhan program.

1.3 Kepentingan Pinjaman Koperasi Kerajaan Malaysia: Memahami kepentingan loan Koperasi Kerajaan Malaysia adalah penting, kerana ia bukan sahaja berfungsi sebagai alat sokongan kewangan untuk kakitangan kerajaan tetapi juga menyumbang kepada pembangunan sosio-ekonomi Malaysia yang lebih luas. Dengan meneliti sejarah evolusi, kriteria kelayakan, proses permohonan, faedah, cabaran dan peraturan kerajaan yang mengelilingi pinjaman ini, kita boleh memperoleh pemahaman yang menyeluruh tentang peranan mereka dalam masyarakat Malaysia.

Loan Koperasi

Evolusi Sejarah

2.1 Kemunculan Koperasi di Malaysia: Gerakan koperasi di Malaysia mempunyai sejarah yang kaya sejak awal abad ke-20. Ia menjadi terkenal sebagai satu cara untuk memperkasakan masyarakat luar bandar dan pengeluar berskala kecil. Prinsip koperasi bantu diri, bantuan bersama, dan kawalan demokrasi telah menjadi sebahagian daripada landskap koperasi Malaysia.

2.2 Peranan Kerajaan dalam Memajukan Koperasi: Kerajaan Malaysia secara konsisten menyokong koperasi melalui dasar, perundangan dan insentif kewangan. Akta Koperasi 1993 menyediakan rangka kerja perundangan untuk pendaftaran dan operasi koperasi di Malaysia. Perundangan ini juga menggariskan komitmen kerajaan untuk mempromosikan sektor koperasi sebagai sarana pembangunan sosio-ekonomi.

2.3 Kejadian Pinjaman Koperasi Kerajaan Malaysia: Pinjaman Koperasi Kerajaan Malaysia muncul sebagai sebahagian daripada usaha kerajaan yang lebih meluas untuk menggalakkan rangkuman kewangan dan pertumbuhan koperasi. Ia mewakili perkongsian strategik antara kerajaan dan koperasi untuk menyediakan pilihan kredit yang berpatutan kepada kakitangan kerajaan. Inisiatif ini selaras dengan Wawasan 2020 Malaysia, yang bertujuan untuk mengubah negara menjadi sebuah negara maju.

Group of Malaysian businesspeople having deals on desk inside office room, businesspeople clapping hands.

Objektif Pinjaman Koperasi Kerajaan Malaysia

3.1 Pemerkasaan Kewangan: Salah satu objektif utama Pinjaman Koperasi Kerajaan Malaysia adalah untuk memperkasakan kakitangan kerajaan dari segi kewangan. Dengan menawarkan akses kepada kredit pada kadar faedah yang kompetitif, program ini membolehkan individu memenuhi pelbagai keperluan kewangan, seperti perbelanjaan pendidikan, perumahan dan kecemasan. Pemerkasaan ini bukan sahaja meningkatkan kesejahteraan penjawat kerajaan tetapi juga menyumbang kepada kestabilan ekonomi.

3.2 Menggalakkan Gerakan Koperasi: Satu lagi objektif utama adalah untuk menggalakkan pertumbuhan koperasi di Malaysia. Dengan menyalurkan dana melalui koperasi, Pinjaman Koperasi Kerajaan Malaysia memperkukuh pertubuhan-pertubuhan ini, yang seterusnya memberi perkhidmatan kepada ahli-ahli mereka dan menyumbang kepada pembangunan ekonomi tempatan.

3.3 Mengurangkan Tekanan Kewangan: Program ini bertujuan untuk mengurangkan tekanan kewangan dalam kalangan kakitangan kerajaan dengan menyediakan sumber kredit yang boleh dipercayai dan boleh diakses. Ia membantu individu mengelak daripada menggunakan pinjaman berfaedah tinggi daripada sumber tidak formal, akhirnya meningkatkan daya tahan dan kestabilan kewangan mereka.

Kriteria Kelayakan

4.1 Kakitangan Kerajaan: Untuk layak mendapat Pinjaman Koperasi Kerajaan Malaysia, pemohon mestilah kakitangan kerajaan. Ini termasuk penjawat awam, guru, profesional penjagaan kesihatan dan pekerja sektor awam yang lain. Program ini direka untuk memenuhi demografi ini secara khusus, mengiktiraf sumbangan mereka kepada perkhidmatan awam.

4.2 Keahlian dalam Koperasi: Pemohon dikehendaki menjadi ahli koperasi berdaftar. Keahlian ini memastikan pinjaman dilanjutkan melalui saluran yang sah dan terkawal. Ia juga menggalakkan gerakan koperasi dengan meningkatkan penyertaan.

4.3 Tempoh Perkhidmatan Minimum: Sesetengah varian Pinjaman Koperasi Kerajaan Malaysia mungkin memerlukan tempoh perkhidmatan minimum sebagai kakitangan kerajaan. Kriteria ini memastikan bahawa pinjaman boleh diakses oleh mereka yang mempunyai sejarah pekerjaan yang stabil dalam sektor awam.

4.4 Sejarah Kredit dan Kapasiti Pembayaran Balik: Pemohon tertakluk kepada penilaian kredit untuk menentukan kapasiti pembayaran balik mereka. Walaupun program ini bertujuan untuk menyediakan bantuan kewangan, amalan pemberian pinjaman yang bertanggungjawab masih dipertahankan untuk mengelakkan keterlaluan berhutang.

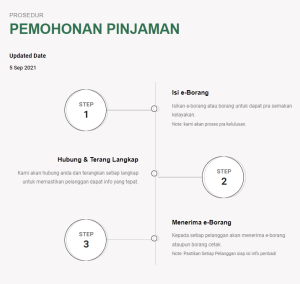

5.1 Dokumentasi Permohonan: Untuk memohon Pinjaman Koperasi Kerajaan Malaysia, pemohon lazimnya perlu mengemukakan pelbagai dokumen, termasuk bukti pengenalan diri, bukti pekerjaan, butiran keahlian koperasi dan penyata kewangan. Keperluan dokumentasi yang tepat mungkin berbeza bergantung pada jenis pinjaman tertentu dan koperasi yang terlibat.

5.2 Saluran Penyerahan: Permohonan biasanya boleh dihantar melalui pelbagai saluran, termasuk portal dalam talian, pejabat koperasi, dan agensi kerajaan yang ditetapkan. Ketersediaan aplikasi dalam talian telah meningkatkan kebolehcapaian dan kemudahan bagi pemohon.

5.3 Proses Kelulusan: Proses kelulusan melibatkan semakan menyeluruh terhadap dokumen pemohon dan kelayakan kredit. Koperasi atau institusi kewangan yang bertanggungjawab untuk mengeluarkan pinjaman menilai risiko yang berkaitan dengan setiap permohonan.

5.4 Pengeluaran Dana: Setelah diluluskan, jumlah pinjaman akan disalurkan ke akaun koperasi pemohon, yang kemudiannya boleh diakses untuk pelbagai tujuan, seperti perbelanjaan pendidikan, perumahan atau kecemasan.

Pinjaman Peribadi Islamik

Jenis Pinjaman Koperasi Kerajaan Malaysia

Pinjaman Koperasi Kerajaan Malaysia menawarkan pelbagai produk pinjaman yang disesuaikan dengan pelbagai keperluan kakitangan kerajaan. Beberapa jenis biasa termasuk:

6.1 Pinjaman Peribadi: Pinjaman peribadi adalah serba boleh dan boleh digunakan untuk pelbagai tujuan, termasuk penyatuan hutang, perbelanjaan perubatan atau pelaburan peribadi.

6.2 Pinjaman Pendidikan: Pinjaman ini direka bentuk untuk menyokong perbelanjaan pendidikan, termasuk yuran pengajian, buku teks dan kos lain yang berkaitan. Ia membolehkan kakitangan kerajaan melabur dalam kemahiran dan kelayakan mereka.

6.3 Pinjaman Perumahan:

Pinjaman perumahan membantu kakitangan kerajaan mencapai pemilikan rumah dengan menyediakan dana untuk pembelian hartanah atau pembinaan rumah. Pinjaman ini selalunya datang dengan kadar faedah yang kompetitif dan syarat pembayaran balik yang menggalakkan.

6.4 Pinjaman Kenderaan: Pinjaman kenderaan membantu kakitangan kerajaan dalam memperoleh kenderaan untuk kegunaan peribadi atau profesional. Mereka memudahkan mobiliti dan keperluan pengangkutan.

6.5 Pinjaman Kecemasan: Pinjaman kecemasan direka bentuk untuk menyediakan bantuan kewangan yang pantas semasa krisis yang tidak dijangka, seperti kecemasan perubatan atau perbelanjaan yang tidak dijangka.

Setiap jenis pinjaman distrukturkan untuk memenuhi keperluan kewangan tertentu, memastikan kakitangan kerajaan mempunyai akses kepada kredit mampu milik untuk pelbagai tujuan.

Kadar Faedah dan Syarat Pembayaran Balik

7.1 Kadar Faedah Tetap lwn. Berubah: Kadar faedah untuk pinjaman Pinjaman Koperasi Kerajaan Malaysia boleh sama ada tetap atau berubah. Kadar tetap menawarkan kestabilan, dengan pembayaran balik bulanan yang konsisten, manakala kadar berubah mungkin berubah-ubah mengikut keadaan pasaran.

7.2 Tempoh Pembayaran Balik: Tempoh bayaran balik berbeza-beza bergantung kepada jenis pinjaman dan terma koperasi. Ia boleh berkisar antara beberapa bulan hingga beberapa tahun, memastikan pembayaran balik sejajar dengan kapasiti kewangan peminjam.

7.3 Tempoh Ihsan: Sesetengah pinjaman mungkin menawarkan tempoh tangguh sebelum pembayaran balik bermula, membolehkan peminjam menumpukan perhatian kepada keperluan mereka sebelum memulakan pembayaran balik. Tempoh tangguh ini amat bermanfaat untuk pendidikan dan pinjaman perumahan.

7.4 Penalti Pembayaran Lewat: Untuk menggalakkan pembayaran balik tepat pada masanya, pinjaman biasanya disertakan dengan penalti untuk pembayaran lewat. Peminjam harus sedar tentang penalti ini dan berusaha untuk memenuhi kewajipan pembayaran balik mereka tepat pada masanya.

Faedah Pinjaman Koperasi Kerajaan Malaysia

8.1 Kadar Faedah Berdaya saing: Salah satu kelebihan Pinjaman Koperasi Kerajaan Malaysia yang paling ketara ialah kadar faedahnya yang kompetitif. Koperasi sering menawarkan kadar faedah yang lebih rendah berbanding bank perdagangan, menjadikan pinjaman lebih berpatutan untuk kakitangan kerajaan.

8.2 Pilihan Pembayaran Balik Fleksibel: Program ini menyediakan pilihan pembayaran balik yang fleksibel, membolehkan peminjam memilih terma yang sejajar dengan kapasiti kewangan mereka. Fleksibiliti ini mengurangkan risiko kemungkiran pinjaman dan tekanan kewangan.

8.3 Rangkuman Kewangan: Dengan menyasarkan kakitangan kerajaan dan bekerjasama dengan koperasi, Pinjaman Koperasi Kerajaan Malaysia menggalakkan rangkuman kewangan, memastikan sebahagian besar penduduk mendapat akses kepada perkhidmatan kewangan formal.

8.4 Kesan Sosial dan Ekonomi: Kesan program ini melangkaui peminjam individu. Ia memupuk pertumbuhan koperasi, yang seterusnya menyumbang kepada pembangunan ekonomi tempatan, penciptaan pekerjaan, dan pemerkasaan komuniti.

9.1 Liputan Terhad: Salah satu cabaran ialah liputan terhad Pinjaman Koperasi Kerajaan Malaysia, kerana ia menyasarkan kakitangan kerajaan terutamanya. Memperluaskan akses kepada segmen penduduk yang lebih luas kekal sebagai cabaran.

9.2 Pinjaman Ingkar dan Pinjaman Tidak Berbayar: Walaupun amalan pinjaman yang bertanggungjawab, sesetengah peminjam mungkin menghadapi kesukaran untuk membayar balik pinjaman mereka. Menguruskan kemungkiran pinjaman dan pinjaman tidak berbayar adalah kebimbangan berterusan.

9.3 Masalah Pentadbiran: Proses permohonan dan kelulusan boleh memakan masa, dan kesesakan pentadbiran boleh menghalang kecekapan program. Memperkemas proses ini adalah penting untuk meningkatkan kebolehcapaian.

9.4 Persaingan dengan Bank Perdagangan: Program ini bersaing dengan bank perdagangan untuk pelanggan, yang mungkin menjejaskan kemampanan dan keuntungan koperasi.

10.1 Kajian Kes Penerima: Beberapa kajian kes menonjolkan impak positif Pinjaman Koperasi Kerajaan Malaysia ke atas individu benefisiari. Kisah-kisah ini mempamerkan bagaimana pinjaman telah membantu kakitangan kerajaan mencapai matlamat kewangan mereka.

10.2 Kesan terhadap Kesejahteraan Kewangan: Penyelidikan dan tinjauan menunjukkan impak positif program terhadap kesejahteraan kewangan kakitangan kerajaan. Ia telah membantu individu menjimatkan wang, mengurangkan beban hutang dan meningkatkan kestabilan kewangan mereka secara keseluruhan.

10.3 Pertumbuhan Koperasi: Pinjaman Koperasi Kerajaan Malaysia telah menyumbang kepada pertumbuhan dan kemampanan koperasi, memupuk rasa pemilikan dan pemerkasaan di kalangan ahli mereka.

Sokongan dan Peraturan Kerajaan

11.1 Peranan Kementerian Pembangunan Usahawan dan Koperasi: Kementerian Pembangunan Usahawan dan Koperasi memainkan peranan penting dalam menyelia dan mengawal selia koperasi di Malaysia. Ia menyediakan bimbingan dan sokongan kepada koperasi, memastikan mereka beroperasi mengikut undang-undang dan peraturan yang berkaitan.

11.2 Rangka Kerja Kawal Selia: Akta Koperasi 1993 menyediakan rangka kerja perundangan untuk operasi koperasi di Malaysia. Perundangan ini menggariskan hak dan tanggungjawab ahli koperasi, struktur tadbir urus, dan pengawasan kawal selia.

11.3 Insentif Cukai: Kerajaan Malaysia menawarkan insentif cukai untuk menggalakkan pertumbuhan koperasi. Insentif ini menggalakkan pelaburan dan penyertaan dalam koperasi, sejajar dengan matlamat pembangunan sosio-ekonomi yang lebih luas.

Analisis Perbandingan dengan Produk Kewangan Lain

12.1 Pinjaman Bank Perdagangan: Pinjaman Koperasi Kerajaan Malaysia berbeza dengan pinjaman bank komersial dari segi kadar faedah, kriteria kelayakan, dan struktur koperasi. Analisis perbandingan akan meneroka kelebihan dan kekurangan kedua-dua pilihan untuk peminjam.

12.2 Institusi Kewangan Mikro: Institusi kewangan mikro juga melayani penduduk yang kurang mendapat perkhidmatan, tetapi model pinjaman dan demografi sasaran mereka berbeza daripada Pinjaman Koperasi Kerajaan Malaysia. Perbandingan akan mendedahkan ciri unik kedua-dua pendekatan.

12.3 Pilihan Simpanan dan Pelaburan Peribadi: Meneliti bagaimana Pinjaman Koperasi Kerajaan Malaysia dibandingkan dengan simpanan peribadi dan pilihan pelaburan akan membantu individu membuat keputusan kewangan yang termaklum. Analisis ini akan mempertimbangkan faktor seperti risiko dan pulangan.

Prospek dan Inovasi Masa Depan

13.1 Kemajuan Teknologi: Penyepaduan teknologi dalam proses permohonan dan kelulusan boleh meningkatkan kebolehcapaian dan kecekapan. Apl mudah alih, platform dalam talian dan dokumentasi digital boleh menyelaraskan operasi.

13.2 Perluasan Kriteria Kelayakan: Meluaskan jangkauan program untuk memasukkan lebih ramai pekerja sektor awam atau memperkenalkan produk pinjaman khusus untuk keperluan yang berbeza boleh diterokai.

13.3 Amalan Lestari: Amalan kemampanan, seperti pembiayaan hijau dan pinjaman beretika, boleh disepadukan untuk sejajar dengan matlamat kemampanan global dan nasional.

Kesimpulan

14.1 Kesan dan Kepentingan: Pinjaman Koperasi Kerajaan Malaysia mempunyai kepentingan yang besar dalam landskap koperasi Malaysia dan kesejahteraan kewangan kakitangan kerajaan. Kesannya terhadap pemerkasaan kewangan, pertumbuhan koperasi, dan pembangunan sosio-ekonomi patut diberi perhatian.

14.2 Cabaran dan Peluang: Walaupun program ini menghadapi cabaran seperti liputan terhad dan kebimbangan kemungkiran pinjaman, terdapat peluang untuk inovasi, pengembangan dan kecekapan pentadbiran yang dipertingkatkan.

14.3 Jalan Hadapan: Masa depan Pinjaman Koperasi Kerajaan Malaysia harus menumpukan pada meningkatkan kebolehcapaian, menggalakkan pinjaman yang bertanggungjawab, dan memanfaatkan teknologi untuk mewujudkan ekosistem kewangan yang lebih inklusif dan mampan untuk kakitangan kerajaan dan koperasi.

Rujukan

Senarai komprehensif rujukan akan disertakan, menampilkan penyelidikan akademik, laporan kerajaan, dokumen dasar dan kajian kes yang menyokong analisis yang dibentangkan dalam dokumen ini.

Analisis terperinci Pinjaman Koperasi Kerajaan Malaysia ini memberikan pemahaman yang menyeluruh tentang sejarah program, objektif, kriteria kelayakan, proses permohonan, faedah, cabaran dan prospek masa depan. Ia menjelaskan bagaimana inisiatif ini menyumbang kepada kesejahteraan kewangan kakitangan kerajaan dan gerakan koperasi di Malaysia, akhirnya memupuk pembangunan sosio-ekonomi negara.

This comprehensive document provides an extensive analysis of Pinjaman Koperasi Kerajaan Malaysia, commonly known as Government Cooperative Loans in Malaysia. The report delves into the historical context, objectives, eligibility criteria, application process, benefits, challenges, and impact of these loans on individuals and the Malaysian economy. With a focus on promoting financial inclusion and socio-economic development, Pinjaman Koperasi Kerajaan Malaysia plays a crucial role in empowering government employees and fostering cooperative movements in the nation.

Table of Contents:

Introduction 1.1 Background 1.2 Objectives 1.3 Significance of Pinjaman Koperasi Kerajaan Malaysia

Historical Evolution 2.1 Emergence of Cooperatives in Malaysia 2.2 The Role of Government in Promoting Cooperatives 2.3 Genesis of Pinjaman Koperasi Kerajaan Malaysia

Objectives of Pinjaman Koperasi Kerajaan Malaysia 3.1 Financial Empowerment 3.2 Encouraging Cooperative Movements 3.3 Alleviating Financial Stress

Eligibility Criteria 4.1 Government Employees 4.2 Membership in a Cooperative 4.3 Minimum Service Period 4.4 Credit History and Repayment Capacity

Application Process 5.1 Application Documentation 5.2 Submission Channels 5.3 Approval Process 5.4 Disbursement of Funds

Types of Pinjaman Koperasi Kerajaan Malaysia 6.1 Personal Loans 6.2 Education Loans 6.3 Housing Loans 6.4 Vehicle Loans 6.5 Emergency Loans

Interest Rates and Repayment Terms 7.1 Fixed vs. Variable Interest Rates 7.2 Repayment Period 7.3 Grace Period 7.4 Late Payment Penalties

Benefits of Pinjaman Koperasi Kerajaan Malaysia 8.1 Competitive Interest Rates 8.2 Flexible Repayment Options 8.3 Financial Inclusion 8.4 Social and Economic Impact

Challenges and Concerns 9.1 Limited Coverage 9.2 Loan Default and Non-Performing Loans 9.3 Administrative Bottlenecks 9.4 Competition with Commercial Banks

Success Stories 10.1 Case Studies of Beneficiaries 10.2 Impact on Financial Well-being 10.3 Cooperative Growth

Government Support and Regulations 11.1 Role of the Ministry of Entrepreneur Development and Cooperatives 11.2 Regulatory Framework 11.3 Tax Incentives

Comparative Analysis with Other Financial Products 12.1 Commercial Bank Loans 12.2 Microfinance Institutions 12.3 Personal Savings and Investment Options

Future Prospects and Innovations 13.1 Technological Advancements 13.2 Expansion of Eligibility Criteria 13.3 Sustainable Practices

Conclusion 14.1 Impact and Significance 14.2 Challenges and Opportunities 14.3 The Way Forward

References

1. Introduction

1.1 Background: Pinjaman Koperasi Kerajaan Malaysia, or Government Cooperative Loans in Malaysia, is a financial assistance program designed to support government employees in the country. These loans are extended through cooperative societies, which are self-help organizations governed by their members. Pinjaman Koperasi Kerajaan Malaysia aims to provide accessible and affordable credit to government servants, promoting financial stability and fostering the cooperative movement in Malaysia.

1.2 Objectives: The primary objectives of Loan Koperasi Kerajaan Malaysia are to provide financial empowerment to government employees, encourage the growth of cooperative societies, and alleviate financial stress among its beneficiaries. This comprehensive analysis will explore how these objectives are achieved and assess the program’s overall impact.

1.3 Significance of Pinjaman Koperasi Kerajaan Malaysia: Understanding the significance of Pinjaman Koperasi Kerajaan Malaysia is essential, as it not only serves as a means of financial support for government employees but also contributes to the broader socio-economic development of Malaysia. By examining the historical evolution, eligibility criteria, application process, benefits, challenges, and government regulations surrounding these loans, we can gain a comprehensive understanding of their role in Malaysian society.

2. Historical Evolution

2.1 Emergence of Cooperatives in Malaysia: The cooperative movement in Malaysia has a rich history dating back to the early 20th century. It gained prominence as a way to empower rural communities and small-scale producers. The cooperative principles of self-help, mutual assistance, and democratic control have been integral to Malaysia’s cooperative landscape.

2.2 The Role of Government in Promoting Cooperatives: The Malaysian government has consistently supported cooperative societies through policies, legislation, and financial incentives. The Cooperative Societies Act of 1993 provides a legal framework for the registration and operation of cooperatives in Malaysia. This legislation also underscores the government’s commitment to promoting the cooperative sector as a means of socio-economic development.

2.3 Genesis of Pinjaman Koperasi Kerajaan Malaysia: Pinjaman Peribadi Koperasi Kerajaan Malaysia emerged as part of the government’s broader efforts to encourage financial inclusion and cooperative growth. It represents a strategic partnership between the government and cooperative societies to provide affordable credit options to government employees. This initiative aligns with Malaysia’s Vision 2020, which aims to transform the country into a developed nation.

3. Objectives of Pinjaman Koperasi Kerajaan Malaysia

3.1 Financial Empowerment: One of the primary objectives of Loan Peribadi Koperasi Kerajaan Malaysia is to empower government employees financially. By offering access to credit at competitive interest rates, the program enables individuals to meet various financial needs, such as education expenses, housing, and emergencies. This empowerment not only enhances the well-being of government servants but also contributes to economic stability.

3.2 Encouraging Cooperative Movements: Another key objective is to promote the growth of cooperative societies in Malaysia. By channeling funds through cooperatives, Pinjaman Koperasi Kerajaan Malaysia strengthens these organizations, which, in turn, provide services to their members and contribute to local economic development.

3.3 Alleviating Financial Stress: The program aims to alleviate financial stress among government employees by providing a reliable and accessible source of credit. It helps individuals avoid resorting to high-interest loans from informal sources, ultimately improving their financial resilience and stability.

4. Eligibility Criteria

4.1 Government Employees: To be eligible for Pinjaman Wang Koperasi Kerajaan Malaysia, applicants must be government employees. This includes civil servants, teachers, healthcare professionals, and other public sector workers. The program is designed to cater specifically to this demographic, recognizing their contribution to public service.

4.2 Membership in a Cooperative: Applicants are required to be members of a registered cooperative society. This membership ensures that the loans are extended through legitimate and regulated channels. It also promotes the cooperative movement by increasing participation.

4.3 Minimum Service Period: Some variants of Pinjaman Uang Koperasi Kerajaan Malaysia may require a minimum service period as a government employee. This criterion ensures that the loans are accessible to those with a stable employment history within the public sector.

4.4 Credit History and Repayment Capacity: Applicants are subject to credit assessments to determine their repayment capacity. While the program aims to provide financial assistance, responsible lending practices are still upheld to prevent over-indebtedness.

5. Application Process

5.1 Application Documentation: To apply for Pinjaman Koperasi Kerajaan Malaysia, applicants typically need to submit various documents, including identification proof, proof of employment, cooperative membership details, and financial statements. The exact documentation requirements may vary depending on the specific type of loan and the cooperative involved.

5.2 Submission Channels: Applications can usually be submitted through multiple channels, including online portals, cooperative offices, and designated government agencies. The availability of online applications has improved accessibility and convenience for applicants.

5.3 Approval Process: The approval process involves a thorough review of the applicant’s documents and creditworthiness. Cooperatives or financial institutions responsible for disbursing the loans assess the risk associated with each application.

5.4 Disbursement of Funds: Once approved, the loan amount is disbursed to the applicant’s cooperative account, which is then accessible for various purposes, such as education, housing, or emergency expenses.

Group of Malaysian businesspeople having deals on desk inside office room, businesspeople clapping hands.

6. Types of Pinjaman Koperasi Kerajaan Malaysia

Pinjaman Koperasi Kerajaan Malaysia offers various loan products tailored to the diverse needs of government employees. Some common types include:

6.1 Personal Loans: Personal loans are versatile and can be used for a wide range of purposes, including debt consolidation, medical expenses, or personal investments.

6.2 Education Loans: These loans are designed to support educational expenses, including tuition fees, textbooks, and other related costs. They enable government employees to invest in their skills and qualifications.

6.3 Housing Loans: Housing loans help government employees achieve homeownership by providing funds for property purchases or home construction. These loans often come with competitive interest rates and favorable repayment terms.

6.4 Vehicle Loans: Vehicle loans assist government employees in acquiring vehicles for personal or professional use. They facilitate mobility and transportation needs.

6.5 Emergency Loans: Emergency loans are designed to provide rapid financial assistance during unexpected crises, such as medical emergencies or unforeseen expenses.

Each type of loan is structured to cater to specific financial needs, ensuring that government employees have access to affordable credit for various purposes.

7. Interest Rates and Repayment Terms

7.1 Fixed vs. Variable Interest Rates: Interest rates for Pinjaman Yuran Koperasi Kerajaan Malaysia loans can be either fixed or variable. Fixed rates offer stability, with consistent monthly repayments, while variable rates may fluctuate with market conditions.